Commodities Lab – Week 5

Energy Stops Dragging Lower, But Metals Start Losing Momentum

For most of this cycle, the portfolio had been benefiting from one very important dynamic: diversification inside commodities was actually working.

Energy was weak, but metals were strong enough to offset it. Gold miners kept momentum alive. Uranium continued trending higher. Industrial metals were still reacting positively to the broader global recovery narrative. That balance is what allowed the portfolio to outperform DBC for several consecutive weeks.

What changed this week

Week 5 changed that dynamic quite a bit. The portfolio is still positive since inception at +2.2%, but the benchmark has now moved ahead to +5.9%, pushing alpha down to -3.7%. More importantly, this is the first week where the portfolio stopped behaving like a diversified commodity basket and started behaving like a portfolio with very concentrated winners and very concentrated losers. And that distinction matters.

Energy remains the main drag

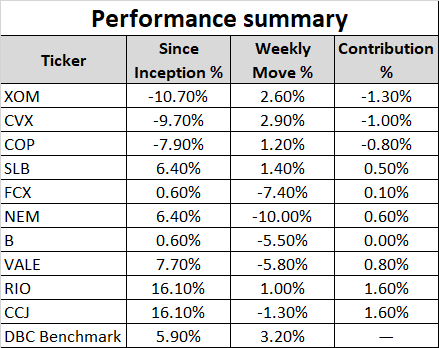

The biggest issue remains energy. ExxonMobil, Chevron and ConocoPhillips all recovered slightly on a weekly basis after several weeks of heavy selling, but the broader damage remains significant. XOM is still down -10.7% since inception, CVX is down -9.7%, and COP remains down -7.9%.

That matters because these are not small tactical positions. Together they still represent more than 30% of the portfolio, so even modest underperformance continues to create a meaningful drag on overall returns.

At the same time, the recovery inside energy still feels tentative rather than structural. Oil equities stabilized this week, but they are no longer leading the commodity complex the way they were expected to at the beginning of the trade.

And that has forced the portfolio to depend much more heavily on metals and mining exposure.

Metals and uranium are still carrying the portfolio

That side of the book is still holding up relatively well. Rio Tinto and Cameco remain the strongest performers in the portfolio, both up +16.1% since inception. Vale continues to work with a +7.7% gain, while uranium exposure remains one of the cleanest trends in the entire portfolio despite a small weekly pullback in CCJ.

The broader mining complex, however, is also starting to lose momentum underneath the surface. Freeport McMoRan gave back a large part of its prior rally and is now only marginally positive since inception at +0.6%. Gold miners also cooled considerably this week after acting as one of the portfolio’s strongest defensive offsets earlier in the move. Newmont dropped sharply from recent highs, though it still holds a respectable +6.4% gain since inception, while Barrick has now almost completely round tripped its earlier advance.

So the portfolio is still positive overall, but the internal structure looks much weaker than it did two weeks ago. That’s really the key point for me.

What I’m seeing now

The market is becoming much more selective inside commodities. Earlier in the move, almost every commodity theme was participating simultaneously. Oil, copper, uranium, gold and industrial metals were all contributing together, which created a very favorable backdrop for a diversified portfolio. That environment is fading.

Now leadership is narrowing considerably. Uranium and diversified miners are still working. Some defensive exposure inside gold is still helping. But energy remains structurally weak, and cyclical metals are becoming far more volatile week to week.

The result is that the portfolio now looks much more dependent on a small number of winners carrying performance. And that’s exactly why alpha collapsed so quickly this week.

The benchmark is benefiting from a broader rebound across the commodity complex, while this portfolio remains heavily exposed to the parts of the market that still haven’t fully recovered, especially large cap oil. That doesn’t necessarily invalidate the original thesis, but it absolutely changes the character of the trade.

Final thoughts

At this point, this is no longer a broad commodity rally. It’s becoming a much more selective environment where positioning and sector allocation matter a lot more than they did at the beginning.